IBOR transition: Resources

Deutsche Bank's IBOR newsletter, timelines on the RFR/IBOR transition, industry news and updates can be found on this page. A glossary of terms used to describe Deutsche Bank's IBOR project is also available.

- November 2022

- August 2022

- April 2022

- January 2022

- December 2021

- October 2021

- August 2021

- June 2021

- April 2021

Timeline of RFR/IBOR reforms

Timeline of RFR/IBOR reforms: Reform for Loans

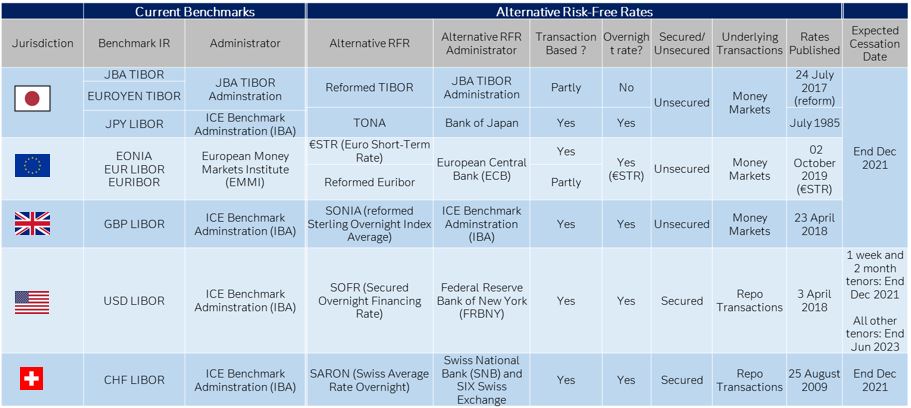

Key attributes for each IBOR and Risk-free Rates

*Transition from IBOR to RFR could bring additional benchmark rates in scope which are indirectly linked to IBOR or use IBOR in the methodology. For example, MIFOR, SOR, etc.

Industry and Regulatory News

Information from the relevant regulators and trade bodies, by currency and geography, can be accessed in the different sections below.

Show content of CHF (Switzerland)

CHF (Switzerland) Document |

Date of publication |

|---|---|

| Swiss financial regulator FINMA publishes LIBOR transition update | September 2021 |

| Revised roadmap shared by FINMA for LIBOR replacement | December 2020 |

| SIX launches SARON Compound indices | March 25, 2020 |

| SNB announces move away from LIBOR | June 13, 2019 |

Show content of Euro (Europe)

Show content of JPY (Japan)

JPY (Japan) Document |

Date |

|---|---|

| Transition of Quoting Conventions in the JPY interest rate swaps market ("TONA First") | August 2021 |

| A $27 Trillion Challenge Looms as Yen Libor Shift Nears | April 2021 |

| Japan debuts swaptions linked to risk-free rate | March 2021 |

| Japan’s JBATA announces retention of JPY TIBOR and cessation of EuroYen TIBOR by December 2024 | March 2021 |

| JFSA and BoJ survey on use of LIBOR | March 13, 2020 |

| BoJ report on use of Japanese Yen benchmarks | November 29, 2019 |

| BoJ announces “Task Force on Term Reference Rates” | August 28, 2019 |

| BoJ consultation on Japanese Yen benchmarks | July 2, 2019 |

Show content of GBP (UK)

Further information can be accessed at the Bank of England facilitated Working Group on Sterling Risk-Free Reference Rates and the FCA’s webpage on Transition from LIBOR websites.

Show content of USD (US)

Information from the Alternative Reference Rates Committee (ARRC)

Show content of Other currencies

Documents for other currencies |

Date: |

|---|---|

| Canadian Alternative Reference Rate Working Group commends decision to cease publication of CDOR | May 16, 2022 |

| MAS Announces Key Initiatives to Support SORA Adoption | August 5, 2020 |

| HKMA letter on reform of benchmarks | July 10, 2020 |

| EMEAP publishes study on the Implications of Financial Benchmark Reforms | September 24, 2019 |

| Singapore banks publish Roadmap for Transition of Interest Rate Benchmark | August 30, 2019 |

| Bank of Canada to become the administrator of key interest rate benchmark | July 16, 2019 |

| ASIC writes to Australian CEOs | May 9, 2019 |

| HKMA writes to CEOs in Hong Kong | March 5, 2019 |